What does a B300 cost?

Private transaction data shows the GPU market still doesn't know what B300s are worth

Listed neocloud rates for B200 and B300 sit within a few percent of each other. Two weeks ago, we argued that parity between B200s and B300s published prices implied a free “option” (in the financial sense) on tomorrow’s workloads. Look at where larger deals actually clear, in the private transaction market, and that idea falls apart.

What buyers actually pay

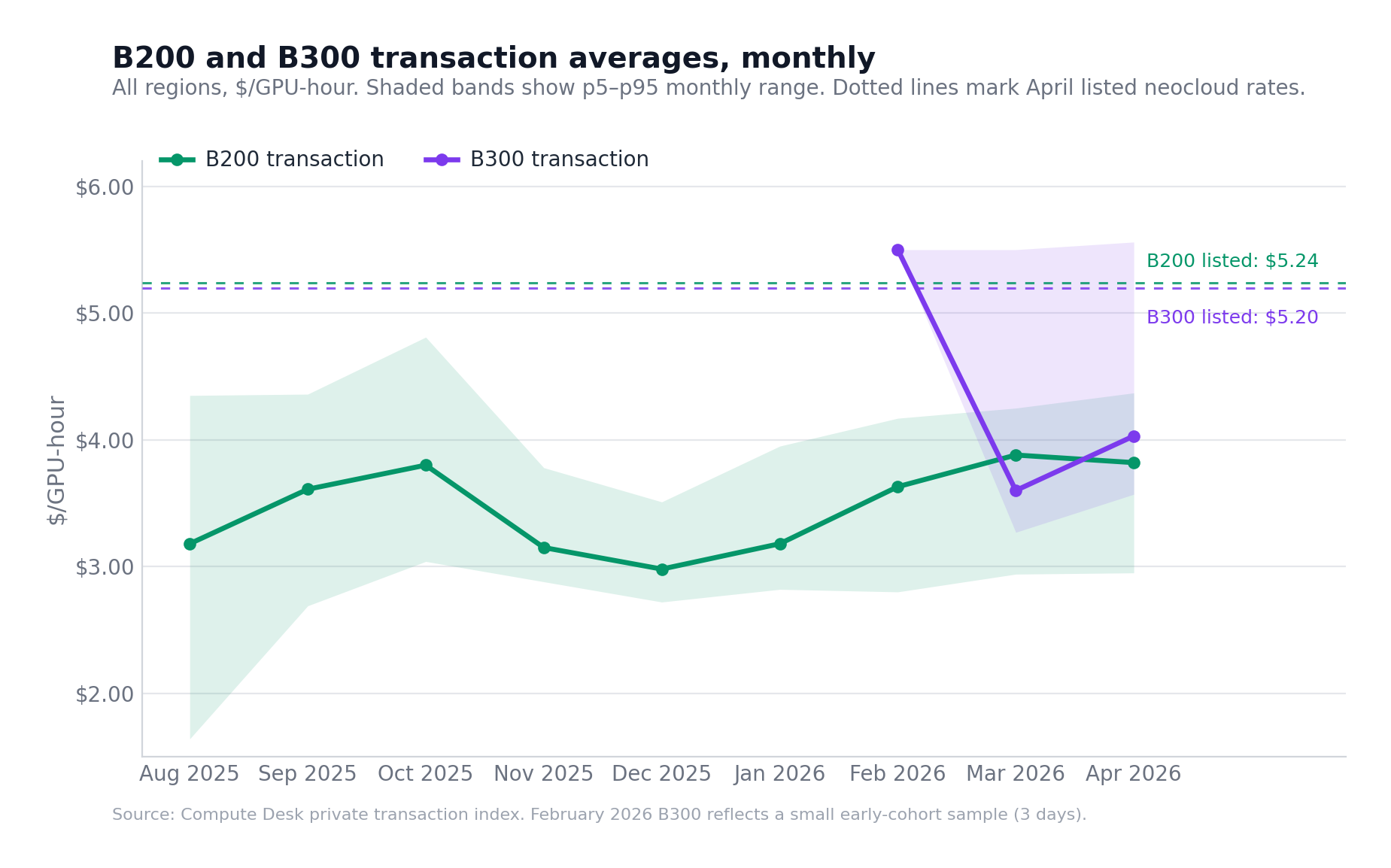

Everything that follows comes from privately negotiated GPU deals, not vendor list prices. The first B300 trades in our private transaction dataset are from late February 2026. We have nine months of B200 transaction data and roughly two months of B300, with about ten weeks of overlap. Here’s how the monthly averages have moved:

Big buyers find more room to negotiate on B200 than on B300, even though listed prices for the two chips are almost identical. In April, B200 averaged $3.82 in private trades against a $5.24 listed rate, a 27% discount. B300 averaged $4.03 against $5.20 listed, a 22% discount. The listed-price story collapses once you look at what buyers actually pay.

The relationship between the two prices is also unstable. B300 has traded above B200, below B200, and above again in the eight weeks since it started trading, currently sitting roughly 25% above. Across 52 days of overlap, it has been cheaper more often than not.

The market doesn’t know what its product is worth

It’s tempting to call this volatility and move on. Don’t. Volatility implies the market is doing its job, just noisily. It isn’t. In a market that works, when prices differ, those differences make sense. A one-year contract should price differently from a one-month contract. A US deal should price differently from a European deal. The same chip from a vendor with worse uptime should sell for less than from a vendor with better uptime. Those differences tell you that the market is sorting trades by their actual characteristics, not just guessing at prices.

But, that isn’t what’s happening here. The wide range of B300 trades, and the way the B300/B200 relationship keeps flipping, is noise from a market that can’t see itself, not a market figuring something out. Buyers don’t know what other buyers paid. Sellers don’t know what other sellers got. There is no public price to compare against.

The chart shows B200’s path: a very wide spread when trading started in summer 2025, a tightening through late 2025, and a widening back out through 2026. Even at its tightest, the range was wider than a transparent market would produce. B300 is somewhere in the early part of that arc. The range of its trades is about as wide as B200’s was a few months in. The number of trades is similar too. The timing fits: B300 only started shipping in late 2025, so the first wave of resale and rental deals is happening now. None of this is surprising.

What we can say is that B300 today looks like B200 looked in its first few months, which is the only point of comparison we have. Two months of data isn’t enough to predict where B300 ends up. What’s clearer is that even after B200 had plenty of volume, its trades still happened across a wide range. That range is itself a measure of how much friction is still in the market.

How to think about buying B300 right now

The honest answer for what a B300 costs right now is a range, and that range has shifted every few weeks for two months. Listed rates show one piece. Private transaction data shows another. Both keep moving. Anyone selling you a single confident number is either marketing or guessing.

B300 is still better than B200 at the workloads AI is moving toward. Better at FP4 inference, the precision more new models are using. Better at serving large mixture-of-experts models, the kind being released this year. Better at long-context production, where B300’s extra memory matters. And the software stack will catch up to B300 over the next year, the way it caught up to B200.

At listed prices, B300 was a few cents an hour cheaper than B200. You got all of those advantages for less money than the older chip. The transaction data complicates that, but not dramatically. In April, B200 cleared around $3.82 an hour and B300 around $4.03. That’s a 21-cent premium for B300. Earlier this year, in late February, the gap was wider, closer to a dollar, but it has narrowed since. Twenty-one cents an hour is not much for hardware that can do things B200 can’t: a 405B dense model on a single GPU, a trillion-parameter MoE on four. If your roadmap is pointed at any of those, B300 is still worth taking. So the procurement question isn’t really “B200 or B300?” It’s “how much B300 can I lock in, and at what price?”

But that only matters if your workload wants B300 in the first place. Which is where price stops being the right starting point. Start with what you’re running. What models do you serve today, and what do you expect to be serving in a year? Are you moving to FP4, and how fast? Is your model roadmap dense, or are you betting on MoE? How long are your context windows getting? Those answers tell you whether B300 is worth a premium at all, and how big a premium you should be willing to pay. A team already serving FP4 inference at scale should treat B300 as essential. A team running dense training with no MoE plans might fairly decide B200 is enough.

Once you know what you’re solving for, look at prices. Both kinds: the listed neocloud rates, and any transaction data you can get hold of. Weight them by what your actual deal looks like. A six-month commitment in Europe will land somewhere different from a one-year deal in Virginia.

Don’t fixate on any single number. Listed rates haven’t kept up with the market. Transaction averages can swing from one window to the next, depending on which deals happened to clear. The right answer this quarter will probably look different next quarter. Plan for that.

Supply alone won’t fix this

Step back from procurement, and the picture is even more troubling. Two GPUs from the same generation, one nine months older, and the price relationship between them has flipped four times in two months. That isn’t a market working. It’s a market that doesn’t know what its own product is worth.

The conventional wisdom is that as B300 supply grows, prices will converge. More vendors, more deals, more meaningful averages. Two months in, the “more vendors, more deals” part is happening. The “more meaningful” part isn’t. What’s missing isn’t more deals. It’s the market structure that lets deals add up to a price: published reference rates, standard contract terms, and shared transaction data. Without those, more deals just produce more noise.

The first piece used listed prices to argue B300 was a free option on tomorrow’s workloads. This piece argues something more uncomfortable: even the prices buyers actually pay are harder to read than they should be. The reason is the same structural gap. B300 will eventually trade in some sensible relationship to B200. Right now it doesn’t, and that uncertainty costs every buyer in the market. Until it does, the only defensible procurement discipline is to monitor where B300 actually trades. That’s what we publish.

Compute Desk publishes private transaction indices for B200, B300, and Hopper-class GPUs across regions and contract types. Reach out if you want to see what your price looks like against the broader market.

The point that more deals without shared price data just produces more noise is one of those observations that feels obvious only after someone says it.