Financial Markets Will Unbundle the Neocloud

Every neocloud today is its own broker, its own insurer, and its own clearinghouse. Not by choice: whatever mix of land, buildings, chips, and contracts a provider owns, every risk attached to them sits on its one balance sheet, because nothing else exists to take any of it. There is no benchmark to price against, no instrument to lay off exposure, no clearinghouse to stand between counterparties. Build that financial layer, and the functions bundled inside every provider today become standalone businesses.

This is a claim about direction, not arrival. Adoption has not happened: no offtake contract references an index, no cleared volume changes hands, no lender underwrites a hedged book. That is why every provider still does it all in-house. Last week’s piece laid out the shapes providers take. This one covers the force that changes them.

Five financial jobs hide inside every provider

Count what a provider does beyond running clusters. Its finance team sets the price, backed out of the cluster’s debt schedule, and reprices it every few months when the model is rebuilt. There is no price discovery in it: a desk with a market view moves with information, a financing model moves when the financing does. Its business development team finds the counterparty and negotiates each deal off that model, one at a time, with no benchmark to reference. Its credit function is the clearinghouse: a multi-year offtake has no central counterparty, so the provider warehouses its customer’s default risk for the life of the deal. Its balance sheet is the insurer, holding price exposure across the asset’s remaining life. And when a customer wants out of committed capacity, the provider improvises the resale, one favor at a time.

None of this is strategy. Each job sits on the provider’s balance sheet because no one else is there to take it: a broker needs a standard contract to trade and a reference price to quote against, and this market has neither; an insurer of price risk needs an instrument to move it; a clearinghouse needs to exist. (Matching is the partial exception: marketplaces do it for a fee. But they hold the thin end of the market, because buyers at scale want contiguous clusters and firm service levels that only a principal controlling the capacity can commit to.)

Buyers carry the mirror image. A reserved-capacity hoard rolls up three different motives: protection against rising prices, certainty that the capacity will be there, and the wish to stay a favored customer when the next generation is allocated. No instrument separates them, so a buyer who mostly wants the certainty pays for all three at once, and reports the whole thing as one line of committed spend.

The hedge replaces the anchor tenant

Untangling all of this runs through the lenders. Today a lender underwrites the offtake contract, so only providers who can sign an anchor tenant can build. A cleared, hedgeable market hands the lender a different package: a clearinghouse in place of the anchor’s credit, a hedge in place of the contract’s term. A provider that could never sign a hyperscaler could still raise debt against a hedged book. More kinds of providers can borrow, and more kinds get built.

This already happened once, in power. The first independent producers raised non-recourse debt against one long-term purchase agreement with one creditworthy utility: one plant, one contract, one counterparty, which is structurally today’s neocloud offtake. Then hubs, benchmarks, and hedges matured, and the quasi-merchant plant became bankable: financed against a forward curve and a hedge instead of a twenty-year contract. Lenders did not become braver. They got instruments. And around the financed plants grew a merchant layer that had never existed under the integrated utility: independent traders, marketers, and brokers, each running one function the utility used to perform in-house. That layer is why capital could reach builders who could never sign a utility, and why risk could sit with whoever wanted it rather than whoever happened to own the plant.

None of it needs to wait for a liquid short-tenor market. Cash-settled contracts settle to an index, not to physical delivery, so the contract can exist wherever an index can be computed, ahead of any liquid market in the underlying. The instrument comes first. In compute it has to, because the liquid short-tenor physical layer does not exist: that was the argument of There Is No GPU Price Hedge, and it still holds.

Once a provider can hand off its price exposure, owning GPUs stops meaning betting on GPU prices. A provider can be long silicon operationally, running clusters at high utilization, without being long price financially. The buyer’s hoard of reserved capacity comes apart the same way. A hedge covers the price. A contract covers the delivery. What is left, staying a favored customer for the next generation, was never a clean purchase anyway, and now stands on its own as a plain bet on the relationship.

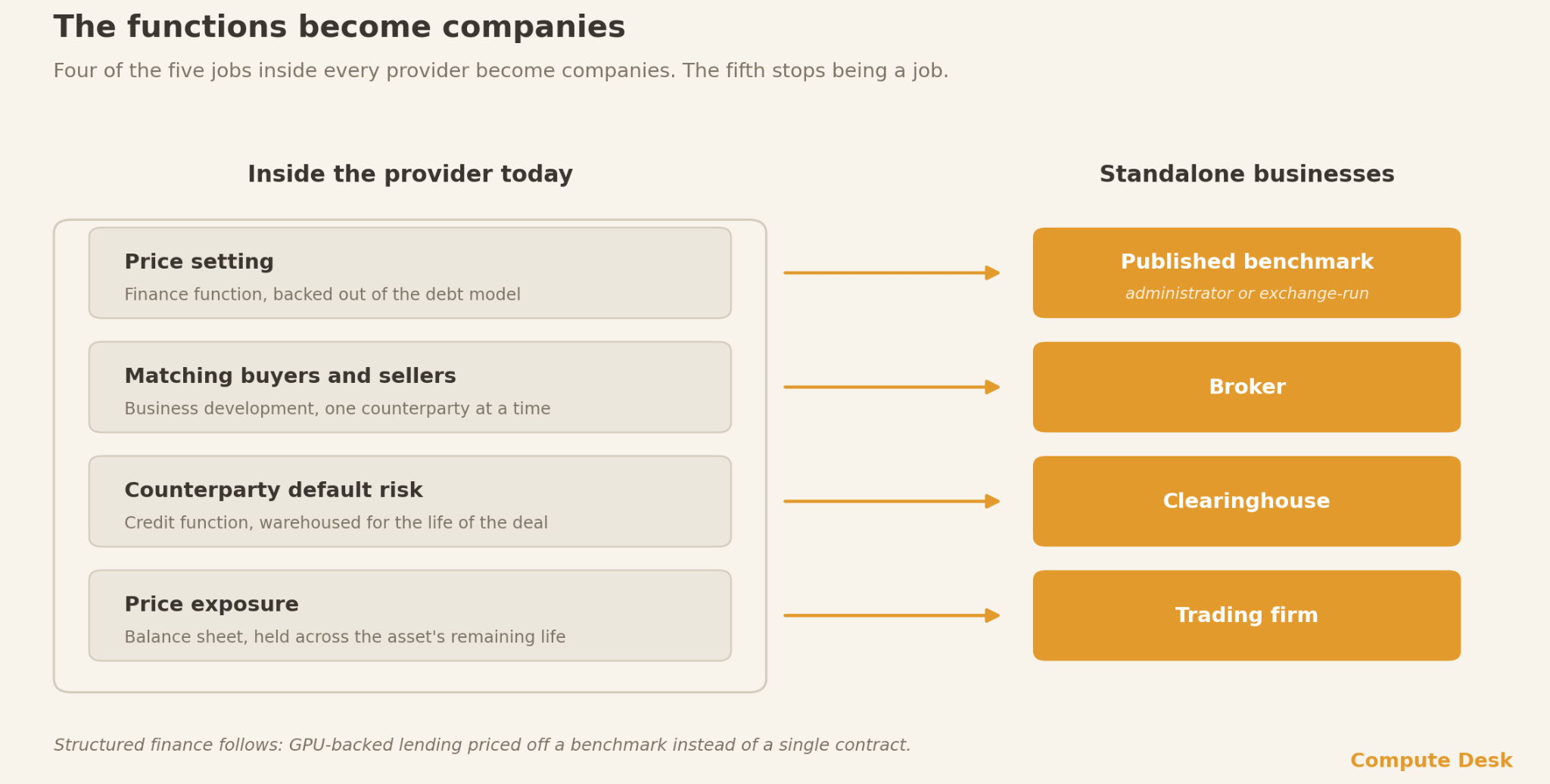

The functions become companies

Four of the five jobs land somewhere as a business. Brokers match buyers with sellers without holding inventory. Clearinghouses stand between buyer and seller, collect collateral from both sides, and absorb a default so that neither side has to underwrite the other. Model-set prices give way to published benchmarks, and the publisher varies: a standalone administrator, or an exchange running its own, as power exchanges do. Trading firms take on price risk deliberately and charge for it, where providers today carry it by default and charge nothing. Structured finance follows: GPU-backed lending priced off a benchmark instead of a single contract.

The fifth job does not relocate. It disappears. Once contracts standardize, getting out of a position is a sale like any other: the same brokers, the same venue, the same clearing. A separate secondary market only exists while every deal is bespoke.

Not everything unbundles. Cluster operations, power procurement, and site development keep real economies of integration, and some power markets never restructured at all: much of the American Southeast still runs vertically integrated utilities. The claim is narrower. The financial functions leave. What stays integrated will stay because the economics favor it, not because no market exists to take the risk.

The financial layer is being built, quickly

The construction has started. Three exchanges have announced plans to list compute futures: Architect, CME Group, and ICE, all cash-settled, all pending regulatory review, with ETF issuers filing products behind them. Architect’s contract settles to our transaction-based index. The markers to watch come in order: bilateral deals priced against an index, cleared volume that counterparties actually rely on, and the first project debt underwritten against a hedged book. Each marker moves risk off a provider’s balance sheet. None has happened yet, but at the pace the announcements are arriving, none looks far away.

Providers already choose their physical position: last week’s spectrum runs from dirt to tokens, and every shape on it is occupied. None of them has had a choice about the financial bundle: the reseller and the integrator alike price off an internal model, warehouse their counterparties’ defaults, and carry the price risk themselves. The financial layer makes it optional: keep the risks that pay and hand off the rest. The companies that take those risks will sit at the center of this market, and they will not need to rack a single GPU.